Summary:

- Credit history is an evaluation of how well you manage debt.

- Credit is impacted by:

- Payment History

- Credit Usage

- Length of Credit History

- Credit Mix

- New Credit

- Credit can be improved by following these 7 steps

- Pay your bills on time

- Prioritize paying off debt with high interest rates or debt that isn’t contributing positively to your Credit Mix (e.g. credit cards, personal loans)

- Pay off credit card balances

- Don’t close long-standing credit cards

- Keep using a small amount of credit and pay it off monthly

- Key into remaining debt: increase payments toward higher than average interest rates

- Keep it up and wait!

What is Credit History?

Credit history is an evaluation of how well you manage debt. Credit history is calculated and described in terms of your Credit Score, which typically falls between 300 and 850. A high credit score indicates responsible debt management which can award you financial opportunity.

Having a high credit score may qualify you for lower interest rates when applying for new credit like mortgages and car loans. You also may qualify for lower interest rate credits cards, increased credit card limits, and/or credit cards with rewards points or cash back. Conversely, a low credit score can be grounds for rejection or higher interest rates when applying for new credit. Credit scores are also often used as a screening factor for home-rental applications, and in some states credit scores are even used as employment screening criteria.

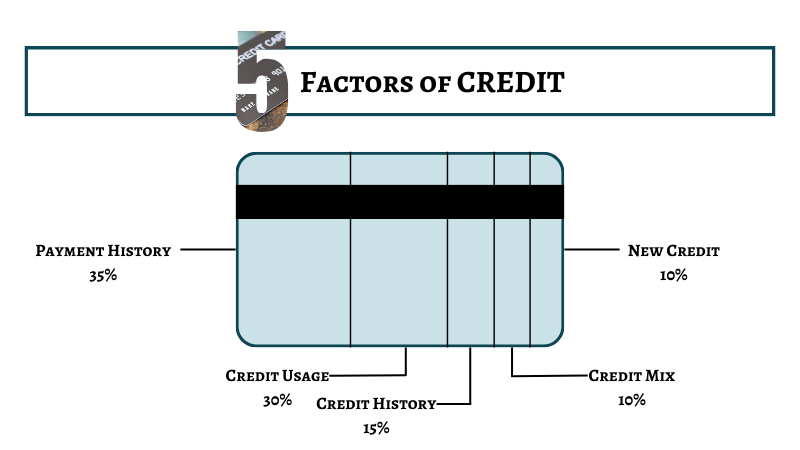

The Five Factors of Credit1

Your credit score is influenced by five factors.

The most influential factor is Payment History, making up 35% of your credit score. Payment History refers to your track record of making on-time payments. There are two types of payments considered: i) repayment of consumer debts and ii) debts sent to collections. The first category includes credit card balance payments, mortgage payments, and other loan repayments. Making on-time payments of this variety is good for your credit score. Debts sent to collections, are the result of unpaid bills, such as an unpaid medical bill. If a bill is sent to collections it will dramatically lower your credit score and generally stay on your credit history for 7 years.

The second most influential factor is Credit Usage, making up 30% of your credit score. Credit Usage refers to how much of your available credit you use, otherwise known as your credit utilization ratio. It is best practice to keep your credit utilization ratio below 30%. For example, you may have a credit card with $1000 of available credit. To maintain a credit utilization ratio of 30% you would only want to utilize up to $300 of the available credit at any given time.

Making up 15% of your credit score is your Length of Credit History. Length of Credit History refers to how long you have been managing credit. If you have a long track record of responsibly managing credit, that positively affects your credit score. Keeping your oldest loans and credit cards open increases the average length of your credit history.

Credit Mix makes up 10% of your credit score. Credit Mix refers to the diversity of your types of credit. For example, you may have a mortgage, car loans, student loans, and various credit cards. Credit scoring favors the ability to manage different types of debt.

Finally, New Credit makes up the remaining 10% of your credit score. New Credit refers to how often you apply for credit. When you apply for a new credit card or loan, the potential lender checks your credit, making what’s called a ‘credit inquiry’. Credit inquiries stay on your credit history for two years. Applying for a lot of new credit in a short period of time can negatively impact your credit.

Seven Steps to Improving Credit

If you are looking to increase your credit score, these seven steps are a great place to start.

- Step One: Make sure you are paying all of your bills on time. This includes making at least the monthly minimum payments on all loans and credit cards, and also making timely payments on all other bills to avoid them being sent to collections. This might mean carrying a balance on your credit card(s) or paying off loans more slowly, but it is important to not miss a payment on any of your accounts.

- Step Two: Prioritize paying off high interest debt that isn’t positively contributing to your credit mix, like credit card debt and personal loans. While accounts like mortgages, car loans, or student loans are often larger loans, they usually have lower interest rates and contribute positively to your credit mix, so paying them off is not as high a priority.

- Step Three: Pay off the balance of your credit cards. Your credit score will immediately increase as soon as your creditor reports your payment to the credit agency. If you’re not able to pay all of your credit card balance(s) at once, put as much of your excess income as possible toward your credit card debt until it is paid off entirely. Do not move to Step Four until all of your credit card debt is paid off.

- Step Four: After you’ve paid off all of your credit card debt, you might be tempted to close all of your credit card accounts. Do NOT close all your credit card accounts at once. Doing so can reduce your length of credit history and your available credit and in turn reduce your credit score again. When choosing which cards to close, close the newest cards or the ones with the lowest available credit limits.

- Step Five: After you’ve paid off all of your credit cards, you may feel trepidatious about using them again. But using your credit cards and paying them off is actually good for your credit. So throw a monthly subscription on autopay with your credit card, and also setup your credit card balance to be paid off in full by your bank account each month. As an added note, be sure to limit your credit use to below 30% of your available credit limit.

- Step Six: Now that your credit cards are in order, it’s time to take a look at the rest of your debt. Managing debt is good for your credit score, so as long as you’re looking to improve or maintain your credit score you want to maintain some debt. Best practice is to continue to make on-time minimum payments on your mortgage, car loan(s), and student loan(s). If any of these loans have higher than average interest rates, you can start making greater-than-minimum monthly payments on those accounts.

- Step Seven: Keep it up! Building or repairing credit takes time, so you’ll need to maintain these credit habits to see improvement.

Do note that everybody’s credit and financial situation is unique. While these steps are a great place to start for improving credit, there may be other strategies available to you. For example, if you have a short length of credit history, it may be advantageous for you to become an ‘authorized user’ on a trusted family member’s long-standing credit card.

My Credit Score is Good, now what?

Maybe you’ve had a long history of good credit, or maybe you recently improved your credit with the steps described above. Regardless of how you got to this point, you might think, “my credit is good, now what?”.

If you plan to continue to use credit in your lifetime, you’ll want to stay the course to maintain good credit. You may have goals like buying a home or car and credit will be a factor in determining your ability to do so – and the cost.

At this point, you may look at ways to protect your credit score. For example, you can freeze your credit to prevent anybody (including you!) from opening new credit accounts in your name. It’s important to note that while your credit is frozen your score can still increase or decrease – so keep up your healthy credit habits for all of your existing accounts!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.