Summary:

- Tax diversification plays a role in your finances when planning for both the present and the future

- Different types of income are subject to different taxes

- Different types of investments are subject to different taxes

- There are multiple strategies related to managing taxes, both in preparing for and living in retirement

When we think of taxes, we often think in terms of what we owe right now or this year. But a thoughtful financial plan balances thinking about the present with planning for the future. With this in mind, let’s talk about tax diversification and the role it plays in financial planning, both for now and for retirement.

Taxes on Various Types of Income

Before we get into the strategies of tax diversification, we need to understand that different types of income come with different taxes.

- Ordinary income or W2 income:

- Is subject to income tax,

- This is a progressive tax where the more you earn, the higher the tax rate is. However if you’re in the 24% tax bracket, that doesn’t mean you pay 24% on all your income. More on tax brackets in a future blog.

- Also subject to payroll taxes like Social Security and Medicare (together called FICA taxes) as well as unemployment, and sometimes state and local payroll taxes.

- Is subject to income tax,

- Various types of business income:

- If you are self employed, your earnings are subject to income tax and self-employment tax.

- The way your business is setup determines how you are taxed (Sole-proprietorship, LLC, S-Corp, C-Corp, etc.)

- Investment income:

- If you sell an investment, the earnings are

- Taxed as income if you held the investment for under a year, or

- Taxed at capital gains tax rates if held for over a year

- If you earn dividends from stocks, they are taxed one of two ways:

- Qualified Dividends are dividends paid by a U.S. corporation or a qualified foreign corporation, and in most cases you must have held the investment for 60 days. These are taxed at the Qualified dividends rate, which is similar to the capital gains rate.

- Non-Qualified (Ordinary) Dividends are all dividends you receive that are not Qualified, and they are taxed at your income tax rate.

- If you earn interest from bonds, CDs, bank accounts, etc., these are usually taxed as income, but there are exceptions.

- If you sell an investment, the earnings are

- Rental income is subject to income tax, but you can deduct certain expenses like mortgage interest, repairs, etc.

- And more!

What Is Tax Diversification?

Tax diversification is the strategy of spreading your savings and investments across accounts that are taxed in different ways:

There are a lot of different ways to invest, and different types of accounts come with their own tax treatment. Some common types of accounts include:

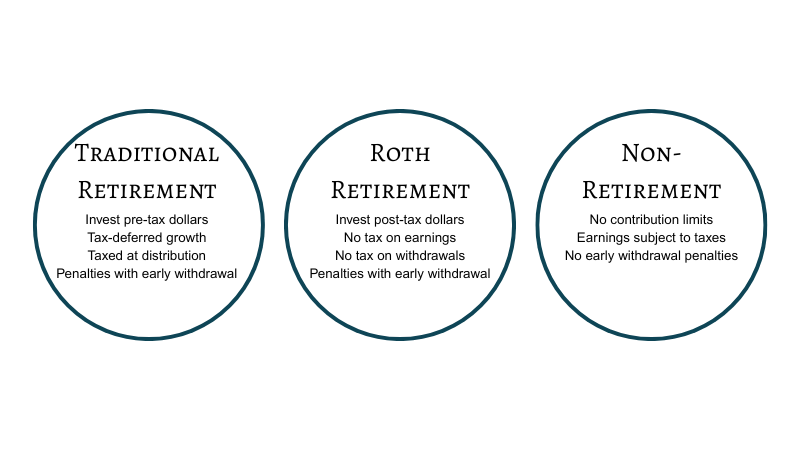

Traditional Retirement Accounts:

Examples: Traditional IRA, Traditional 401(k), SEP IRA

You contribute pre-tax dollars, your investments grow tax-deferred, and you pay ordinary income tax when you withdraw the funds later. There are also potential penalties if you withdraw these funds too early.

Roth Retirement Accounts:

Examples: Roth IRA, Roth 401(k)

You’ve already paid taxes on the funds that you contribute to the account, which means that the earnings grow tax-free, and when you eventually take withdrawals, they are tax-free. As these are also retirement accounts, there are also potential penalties if you withdraw these funds too early (but there are exceptions).

Non-Retirement/Taxable Accounts:

Examples: Other investment accounts, savings accounts, CDs

These are generally taxed each year based on what you earn or sell:

If you sell an investment for more than you bought it for, the profit is taxed as a capital gain.

If you lose money on an investment, you may be able to use that to lower your taxes.

There is also something to be aware of called a Step Up in Cost Basis:

The cost basis of an asset is the value that is used to decide what the gains (or losses) are if you sell that asset. It usually starts as the purchase price of the asset.

When someone passes away and leaves an asset like a house, stock, or investment account to a beneficiary, the cost basis of that asset is usually “stepped up” to its fair market value on the date of death. This step-up can reduce or eliminate capital gains taxes if the beneficiary later sells the asset.

For example, if you buy a house for $100,000 and then sell it for $1,000,000 you’ll have to pay taxes on $900,000 (ignoring other exclusions, etc). However, if you passed away when it was worth one million and then your beneficiary sold it, they wouldn’t have to pay any taxes, because the cost basis “stepped up” to one million.

This doesn’t affect retirement accounts, because retirement accounts are taxed as income (or not taxed at all). Their tax isn’t based on the gain in the account.

Other Accounts:

Health Savings Accounts offer savings and growth potential to reserve and build funds for the purpose of medical expenses later in life. Contributions to these accounts are tax deductible, earnings grow tax-free, and distributions are not taxed if they are used for qualified medical expenses.

529 Plans are a vehicle for investing funds to be used for a beneficiary’s education expenses. Earnings grow tax-free and withdrawals are tax-free if used for qualified education expenses.

o Annuities can defer taxes. For example if you have a four year annuity that pays 4%, you won’t have to pay taxes on the 4% each year. However you will have to pay taxes at the end of the 4 years.And more!

Tax diversification means having a mixture of these various types of accounts, depending on both your short and long term goals. You may wonder if a Roth is always superior to Traditional, or vice versa, but the truth is that it depends on your goals, and usually a mix of all types of investments is the approach we land on. Remember, it’s about strategizing immediate tax savings balanced with preparing for a variety of future, unpredictable tax scenarios.

Where and How you Contribute Funds

There are several tax-tactics we can deploy to get tax-savvy even after you’ve started investing. Some of these methods are:

· Roth conversions:

A Roth conversion is when you move money from a pre-tax retirement account (like a traditional IRA or 401(k)) into a Roth IRA. You’ll pay income tax on the amount you move for the year you move it, but you won’t have to pay taxes on earnings or future qualified withdrawals. One example of when this might make sense is if you predict that your current tax bracket is lower than your future tax bracket.

· Tax loss harvesting:

is a strategy where you sell an investment at a loss and it in turn reduces your tax bill. The loss can be used to offset gains from other investments or even reduce some of your regular income.

· Capital gain harvesting:

Capital gain harvesting is the strategy of intentionally selling investments at a time when you’re in a low tax bracket. It may sound odd to choose to pay taxes, but in certain scenarios you can actually pay a 0% tax rate, reset your cost basis, and reduce future taxes.

· And more!

Why Does Tax Diversification Matter?

At first glance, it might not seem like a big deal. After all, you’ll pay taxes either way, right? But when you pay taxes can make a significant difference in your long-term financial outcome.

Here are three examples of tax diversification at work:

· Flexibility in Retirement:

Having different tax “buckets” to pull from allows you to manage your taxable income in retirement.

Let’s say one year you have a large expense like a home repair or a family vacation, and you need to withdraw more than usual. Instead of pulling it all from your traditional IRA (and potentially pushing yourself into a higher tax bracket), you could supplement with a tax-free Roth withdrawal or a capital gains withdrawal from your brokerage account.

This gives you more control over your taxable income year by year, which can also help you avoid Medicare premium surcharges and other income-based costs.

· Long-Term Tax Planning

Having only tax-deferred accounts (like a 401(k) or traditional IRA) may seem fine while you’re working, but once you turn 73 (or 75 depending on your birth year), you’re required to start taking required minimum distributions (RMDs).

These forced withdrawals can bump you into higher tax brackets and limit your ability to manage income. But if you’ve also saved in a Roth IRA or taxable account, you’ll have more levers to pull to reduce the impact of RMDs.

Plus, tax diversification gives you more options if tax laws change—which they will. Having money in multiple types of accounts is a hedge against rising tax rates.

· Improved Legacy Planning

Tax diversification isn’t just about your lifetime, it can affect how much your heirs receive, too.

For example, inherited Roth IRAs can be withdrawn tax-free by beneficiaries, while inherited traditional IRAs require taxes to be paid (often over just 10 years under the SECURE Act rules). And as discussed above, assets not held in retirement accounts get a step up in their cost basis at the time of the owners death, meaning your beneficiaries won’t have nearly as many taxes to pay when they decide to sell.

Having a mix of account types allows for more strategic gifting and estate planning. It’s a valuable way to extend your impact across generations.

The Bottom Line

You don’t need to predict future tax laws or overhaul your finances overnight. Tax diversification is about giving your future self the flexibility to adapt, optimize, and make tax-efficient decisions based on what’s happening in your life and with the IRS.

There’s more to tax strategy than we’ve even covered in this blog, we didn’t even talk about estate-taxes, gift-taxes, or qualified charitable distributions! But if you need help with planning your tax approach, reach out to us and we can talk specifics.

Important Disclosures:

Content in this article is for general information only and not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

A Roth IRA offers tax deferral on any earnings in the account. Qualified withdrawals of earnings from the account are tax-free. Withdrawals of earnings prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Limitations and restrictions may apply.

Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

This blog was written with the assistance of Artificial Intelligence, specifically Chat GPT.